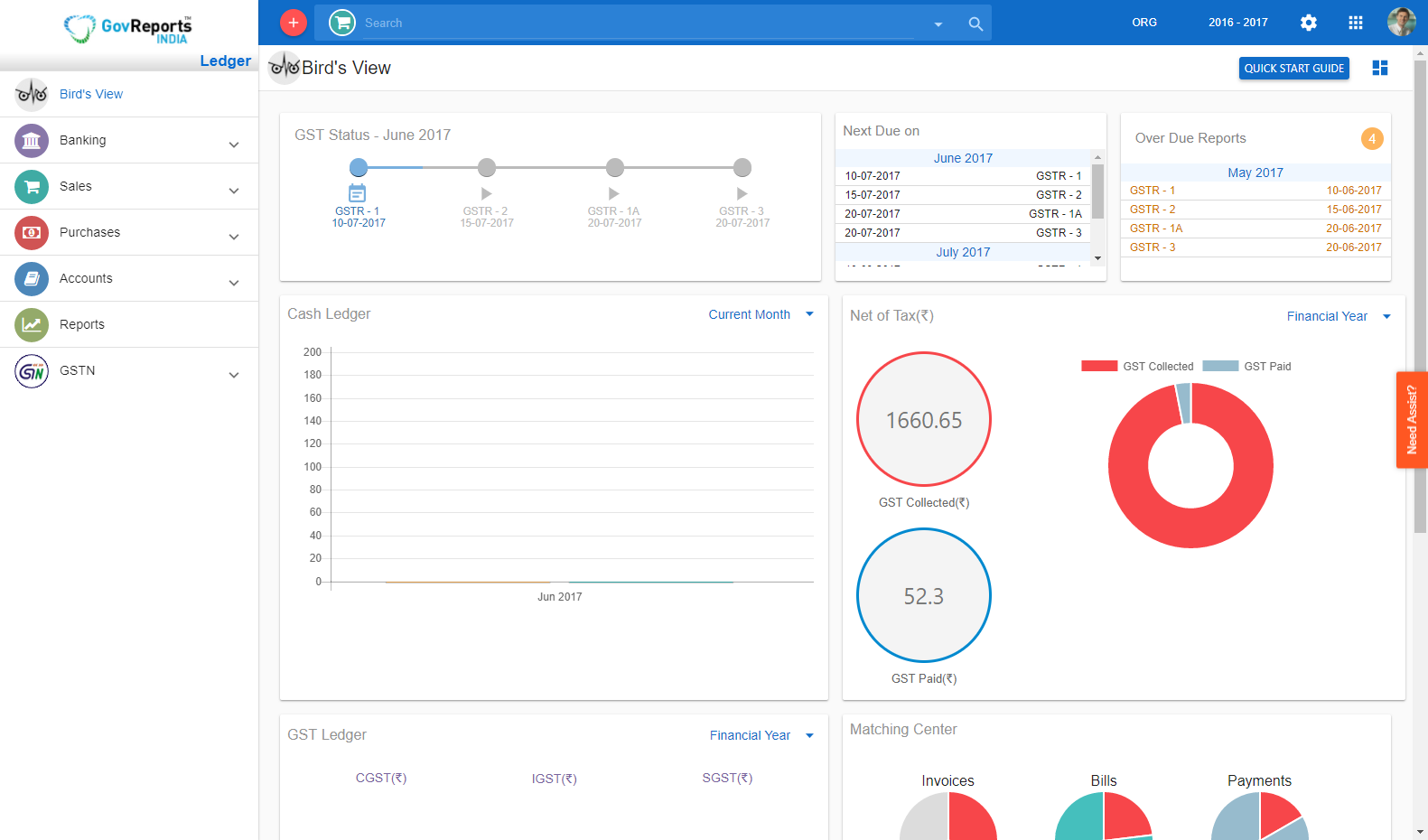

GST Reconciliation of Electronic Ledgers

When accountants identify and work on reconciliation means the books on the business should reconcile with the counter business event. Similar to 'Bank Reconciliation' or 'Fixed Assets Reconciliation', GST reconciliation follows the same process with the extension as every data recorded is converted in to digital form.

In GST reconciliation, any originated business transaction has to match exactly with responding business transaction. When reconciliation is achieved, the amount recorded as well as all GST compliant properties of the transaction will match.

Reconciliation means matching all supplies, purchases and cash transactions data with the other parties involved in the transactions. But when it comes to electronic ledgers, the business should be more cautious in originating supply tax invoice, entering a bill of purchase or posting a cash entry as part of GST transactions.

Supply of Tax Invoice as well as entering the purchase/expense bills has to be done with utmost care, conforming to all GST compliance. Any single point of deviation or mistake, say Tax Invoice Serial Number, could push the transaction to the mismatch items.

Entering Bills with the intention to reverse charge could be another challenge for the businesses. Reversing charged GST need to be declared as tax liability as well as input tax credit. This will have an impact on both electronic liability ledger and electronic input tax credit ledger.

Books should be posted with the penalties, interests, fees and other charges levied by GSTN. These entries should be posted by an auto posting method, so that the reconciliation part will take care on its own.

Businesses will not be required to do much on GST reconciliation, as long as it manages the data as a natural flow of the respective transactions.